Huntsman (HUN)·Q4 2025 Earnings Summary

Huntsman Q4 2025: EPS Miss Sends Stock Down 9% as Polyurethanes Struggles

February 17, 2026 · by Fintool AI Agent

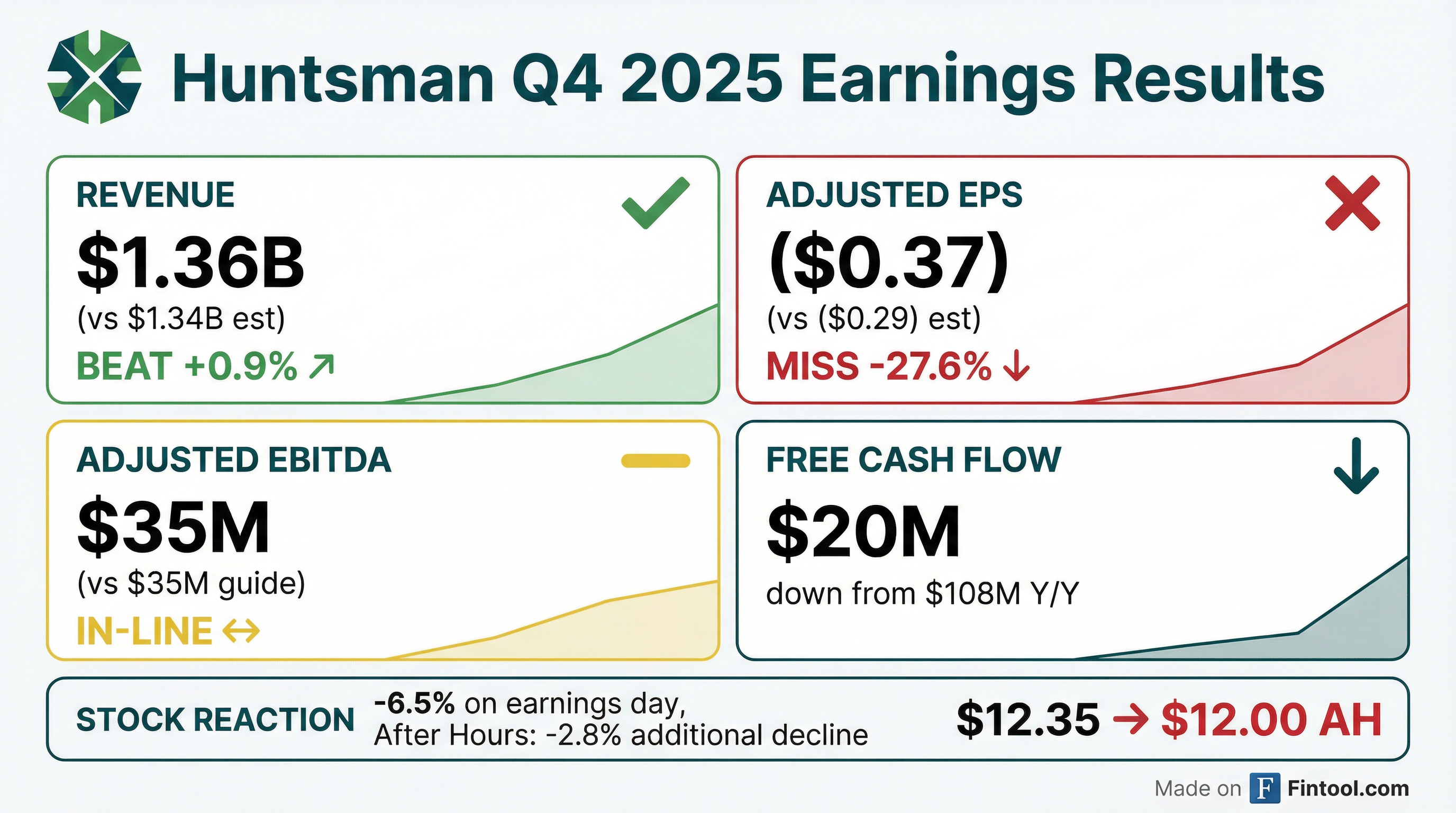

Huntsman Corporation (NYSE: HUN) reported Q4 2025 results that fell short of expectations, with adjusted EPS of -$0.37 missing consensus by $0.08 despite a marginal revenue beat . The stock plunged 6.5% on the day and fell another 2.8% in after-hours trading, reflecting investor disappointment with continued Polyurethanes weakness and a muted near-term outlook. The company's largest segment saw adjusted EBITDA cut in half year-over-year, underscoring the challenging environment in specialty chemicals.

Did Huntsman Beat Earnings?

Revenue: Slight beat. $1.355B vs $1.343B consensus (+0.9%)

Adjusted EPS: Miss. -$0.37 vs -$0.29 consensus (-27.6% worse)

Adjusted EBITDA: In-line with lowered guidance. $35M vs $25-50M guided range (came in at the midpoint after Rotterdam outage pushed expectations to low end)

The revenue beat was largely offset by significant margin compression, particularly in Polyurethanes where the Rotterdam outage compounded already weak market conditions. This marks Huntsman's fourth consecutive quarterly loss on an adjusted basis.

How Did the Stock React?

Earnings Day Move: -6.5% ($13.21 → $12.35)

After-Hours: -2.8% additional decline ($12.35 → $12.00)

Total Impact: ~9% decline

Huntsman's stock sold off sharply despite the modest revenue beat, as investors focused on:

- The EPS miss and margin deterioration

- Polyurethanes segment EBITDA collapsing 50% Y/Y

- Conservative Q1 2026 guidance suggesting no near-term recovery

- Credit rating downgrade to below investment grade (Ba1/BB+/BBB-)

The stock is now trading near its 52-week low of $7.42, having fallen 33% from its 52-week high of $18.04.

What Changed From Last Quarter?

Q3 2025 → Q4 2025 Key Changes:

The sequential deterioration was more pronounced than typical seasonality. Key drivers:

- Volume weakness: Sales volumes declined 2% Y/Y with pronounced softness in Europe

- Price & mix headwinds: Negative $116M impact Y/Y from pricing pressure

- Rotterdam outage: ~$5M EBITDA drag from unplanned facility shutdown

- European construction: Continued weakness in key end-markets

What's Happening in Each Segment?

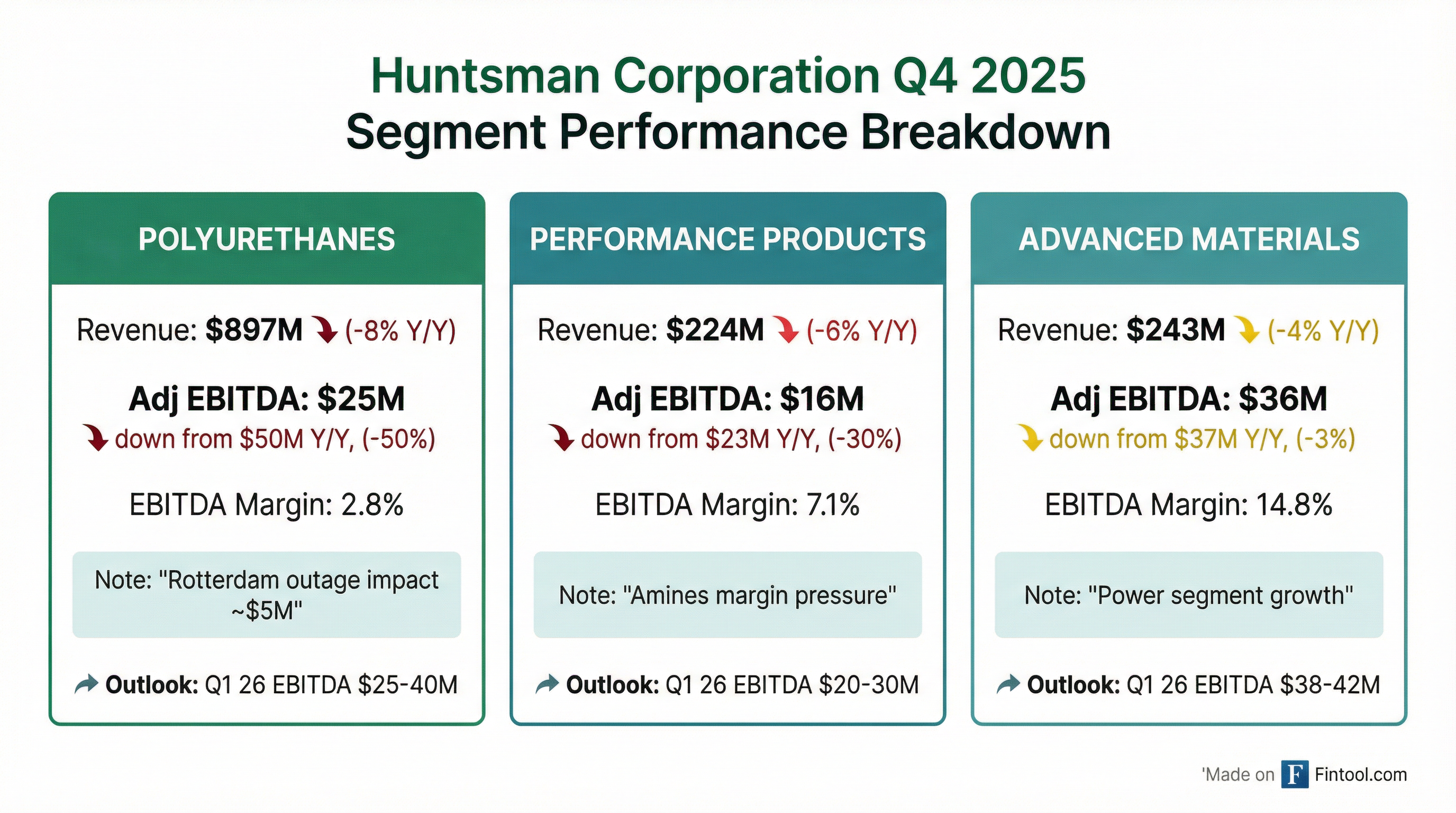

Polyurethanes — The Problem Child

The flagship Polyurethanes segment (65% of revenue) delivered disappointing results :

- Volumes +2% Y/Y with growth in Americas/Asia offset by European weakness

- Rotterdam outage reduced EBITDA by ~$5M

- Chinese MTBE JV delivered only marginal equity income contribution

Q1 2026 Outlook: $25-40M adjusted EBITDA — volumes typically lower seasonally, but cost savings program benefits and some pricing improvement expected .

Performance Products — Margin Compression

Performance Products faced continued amines margin pressure from unfavorable supply/demand dynamics . Volumes excluding EU maleic anhydride actually grew ~2%.

Q1 2026 Outlook: $20-30M adjusted EBITDA — near-term construction headwinds persist, Fuel & Lubes markets stable .

Advanced Materials — Relative Bright Spot

The most resilient segment maintained margins near prior year levels despite revenue pressure . Power end-market showed Y/Y growth while aerospace, coatings, and industrial markets remained soft.

Q1 2026 Outlook: $38-42M adjusted EBITDA — improved aerospace sales expected Q/Q, continued Power strength .

What Did Management Guide?

Q1 2026 Adjusted EBITDA Guidance: $45-75M

Key Assumptions:

- Market conditions remain challenged

- Soft but stable global construction with seasonal improvements ahead

- Y/Y growth in aerospace and power; automotive relatively flat

- European MDI pricing improvement offset by higher natural gas and benzene

- Continued cost savings program benefits

Cost Realignment Update

Huntsman is executing on its ~$100M run-rate cost savings program :

2026 Expected In-Year Savings: ~$45M (excluding inflation impact)

Site closures announced include Boisbriand, Kings Lynn, Deggendorf, Dubai (Polyurethanes), Moers (Performance Products), East Lansing (Advanced Materials), and Frankfurt (Shared) .

Balance Sheet and Liquidity

Leverage increased significantly as EBITDA contracted. Credit ratings were downgraded to below investment grade at Moody's and S&P in Q1 2026 .

New Credit Facility: On February 9, 2026, Huntsman entered a new $800M senior secured revolving credit facility (replacing prior 2022 agreement) with an option to increase commitments by up to $400M .

Dividend: Cut to $0.0875/share (from $0.25/share in Q4 2024) reflecting cash preservation priorities .

2026 Key Action Priorities

Management outlined three strategic priorities for 2026 :

1. Growth & Innovation

- Y/Y growth in MDI volumes including automotive innovation benefits

- Realize benefits from recent capital investments

- Advanced Materials growth in aerospace, power, and Miralon® development

2. Cash Management

- Maintain disciplined capital allocation

- Generate free cash flow in excess of dividend

- Drive further cash conversion cycle improvement

3. Cost Management

- Capture savings from announced cost programs

- Exit remaining restructuring-related sites

- Operational productivity improvements to offset inflation

Full Year 2025 Summary

Despite the earnings deterioration, Huntsman improved cash flow conversion through working capital management and lower capital intensity. This provides some cushion as the company navigates the challenging market environment.

2026 Modeling Considerations

What to Watch

- European MDI pricing recovery: Key driver for Polyurethanes margin expansion

- Rotterdam facility operations: Any further disruptions would pressure Q1 results

- Construction end-market stabilization: Particularly in Europe where weakness persists

- Cost savings execution: ~$45M of in-year benefits expected in 2026

- Leverage trajectory: Net debt/EBITDA at 5.8x needs to decline to avoid further credit actions